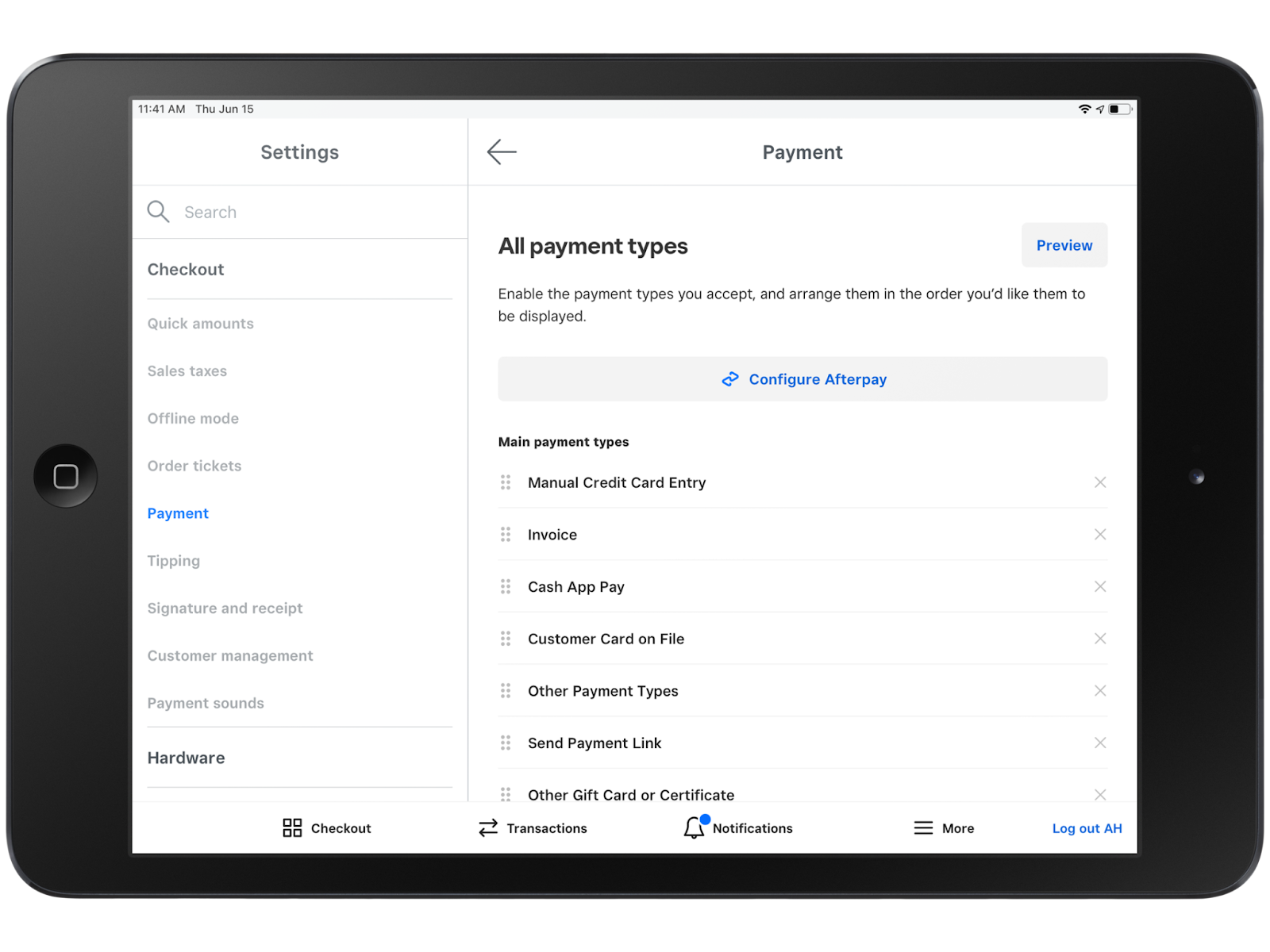

The best online payment processors provide you with varied payment methods such as online checkout pages for accepting credit card payments through websites, digital invoicing, virtual terminals, mobile wallets, and even manual payment methods (like keyed-in transactions).

I have reviewed dozens of payment processors and curated the top providers below.

SPONSORED

Software Spotlight: PaymentCloud

Flexible payment processing for any business

- 98% of applications are approved for a merchant account

- Wide range of payment options – including no-cost (surcharging)

- Month-to-month contract

- No setup, application, or annual fees

Visit PaymentCloud

What is An Online Payment Processor?

A payment processor handles all the steps needed to ensure payment transfer. It helps businesses accept varied payment methods securely and quickly and transfers funds from the customer’s account to the business’s account.

Best Online Payment Processors At A Glance

Product

Our Score (out of 5)

Monthly Fee (starts at

Online Payment Fee

Invoicing

Virtual Terminal

Stripe

4.54

$0

2.9% + 30 cents

Incurs extra costs

Yes

Authorize.net

4.50

$25

2.9% + 30 cents

Yes – Single and recurring

Yes

Helcim

4.48

$0

Interchange plus 0.15% + 15 cents to 0.50% + 25 cents

Yes – Single and recurring

Yes

Square

4.42

From $0

2.9% + 30 cents

Yes – Single and recurring

Yes

Shopify

4.29

From $5

2.9% + 30 cents

Yes – Single and recurring

Yes

PayPal

4.27

$0

2.59%–2.99% + 49 cents

Recurring incurs extra costs

Incurs extra costs

Chase

4.20

From $0

2.9% + 25 cents

Yes – Single and recurring

Yes

CardX

3.51

From $29

From 2.91%

Yes – Single and recurring

Yes

Stripe: Best overall, customization, and multi-currency payments

Overall Reviewer Score

4.54/5

Pricing & Contract

4/5

Payment Types

4.72/5

Sales & Account Management Features

4.53/5

User experience

5/5

User scores

4.47/5

Pros

- Highly customizable checkout options

- Can process transactions in 135+ currencies

- Great API and hundreds of integrations

Cons

- Limited functionality for in-person sales

- Requires coding and developer skills for customization

- Add-on fees for recurring billing and invoicing

Why I chose Stripe

Stripe is a highly favored and popular payment processor that is also part of our recommended payment gateways and merchant services. It accepts dozens of payment methods online and transacts in more than 135 currencies. B2B businesses, in particular, can benefit from its invoicing tool and inexpensive ACH transaction fees—the lowest among the software in this list (0.8%, $5 cap), except for Helcim (zero fees).

What I like about Stripe is that, in addition to its varied accepted payment methods, its checkout customizability can’t be beat. It has the most integrations among the providers I have evaluated in this list, and its online knowledge base and APIs are a clear favorite of developers in the reviews I have read.

- Payment methods: A few standout payment methods include:

- Cross-border payments: Process multiple payment methods using local payment services from other countries. Customers can pay in their local currency and you receive payments converted to your own. It is available in 47 countries and accepts more than 135 currencies.

- Stripe Checkout: Stripe has its own hosted checkout page which you can customize further. Stripe Checkout can be set up for one-time or subscription payments.

- Payment links: Send payment links to collect payments or donations, sell services or products, or start a subscription. Post these links on social media or via SMS or email directly to customers.

- Manual payments: Process payments using a virtual terminal available in your Stripe dashboard. This also lets you receive payments by phone or use a customer’s stored payment details.

- Stripe Connect and Stripe Apps: Stripe offers hundreds of applications and custom APIs and SDKs for easy integration.

- Encryption: Stripe is certified at the highest level of security under PCI DSS (Payment Card Industry Data Security Standards)—PCI Service Provider Level 1.

- Stripe Identity: These are tools that can help create varied types of identity verification methods.

- Stripe Radar: This machine-learning fraud prevention tool includes advanced payment, hardware and account protection tools, and secure data migration.

- Monthly fee: $0

- Ecommerce: 2.9% + 30 cents

- Card-present: 2.7% + 30 cents

- Keyed-in: 3.4% + 30 cents

- Contactless: 2.9% + 30 cents

- Tap-to-pay on mobile: +10 cents per authorization

- Virtual terminal: 2.9% + 30 cents

- ACH: 0.8%, $5 cap

- Invoicing: +0.4%–0.5%

- Recurring billing: + 0.5%–0.8%

- International payments: + 1.5% fee, 1% spread for currency conversion

- Stripe Checkout: $10 per month if using custom domain

- Chargeback fee: $15

- Deposit: 2 business days

- Instant payout: 1%, minimum 50 cents for instant payout

Authorize.net: Best payment gateway

Overall Reviewer Score

4.50/5

Pricing & Contract

4/5

Payment Types

4.72/5

Sales & Account Management Features

4.38/5

User experience

5/5

User scores

4.4/5

Pros

- Works as a payment gateway and payment processor

- 24/7 live support

- All-in-one option includes a third-party merchant account

Cons

- Outdated user interface in the admin dashboard

- Lacks some in-person payment features

- Limited reporting tools

Why I chose Authorize.net

Authorize.net is my top recommendation for a payment gateway—it topped my evaluation of over a dozen payment gateways. But what I like about this provider is the flexibility it offers in terms of how you use its services, whether as a full payment processor or just as a payment gateway and go with a different merchant account.

If you go with its all-in-one solution (gateway and processor), you can accept all remote transactions such as cross-border, B2B payments, invoicing, and recurring transactions. Authorize.net accepts all payment types, including PayPal, and can easily integrate with leading ecommerce platforms.

- Robust payment toolkit: Authorize.net can process online and in-person payments, credit cards, ACH, e-checks, mobile wallets, and invoices. Subscriptions or recurring billing can also be supported.

- Virtual terminal: This terminal can accept payments over the phone or email and can also process level 2 data (B2B transactions).

- Integrations: Authorize.net is partnered with 160 software development platforms, integrates with 145 systems (from POS hardware to accounting systems), and has open API for third-party and custom-built technologies.

- Customer Information Management (CIM): Save cards on file and billing and shipping information for customers (up to 10 payments for each profile) to make easier purchases.

- Advanced fraud protection: The platform’s Advanced Fraud Detection Suite (AFDS) has 13 rules-based filters and tools to identify, manage, and prevent suspicious and potentially fraudulent transactions.

The all-in-one plan includes an Authorize.net partner merchant account and payment gateway.

- Monthly fee: $25

- Setup fee: $0

- Transaction fee: 2.9% + 30 cents

- International payments: 1.5% per transaction

- ACH: 0.75% per transaction

- Verbal authorization: $1.20 per transaction

- Chargeback fee: $25

- Payout: 24 hours (no fees)

- Included: recurring billing service, fraud detection, customer management

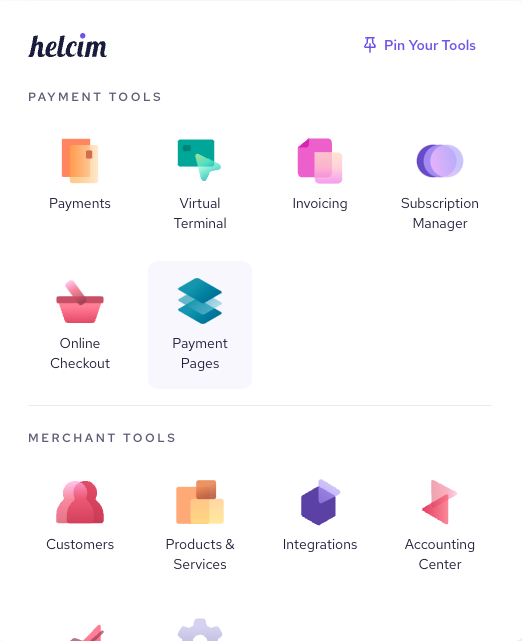

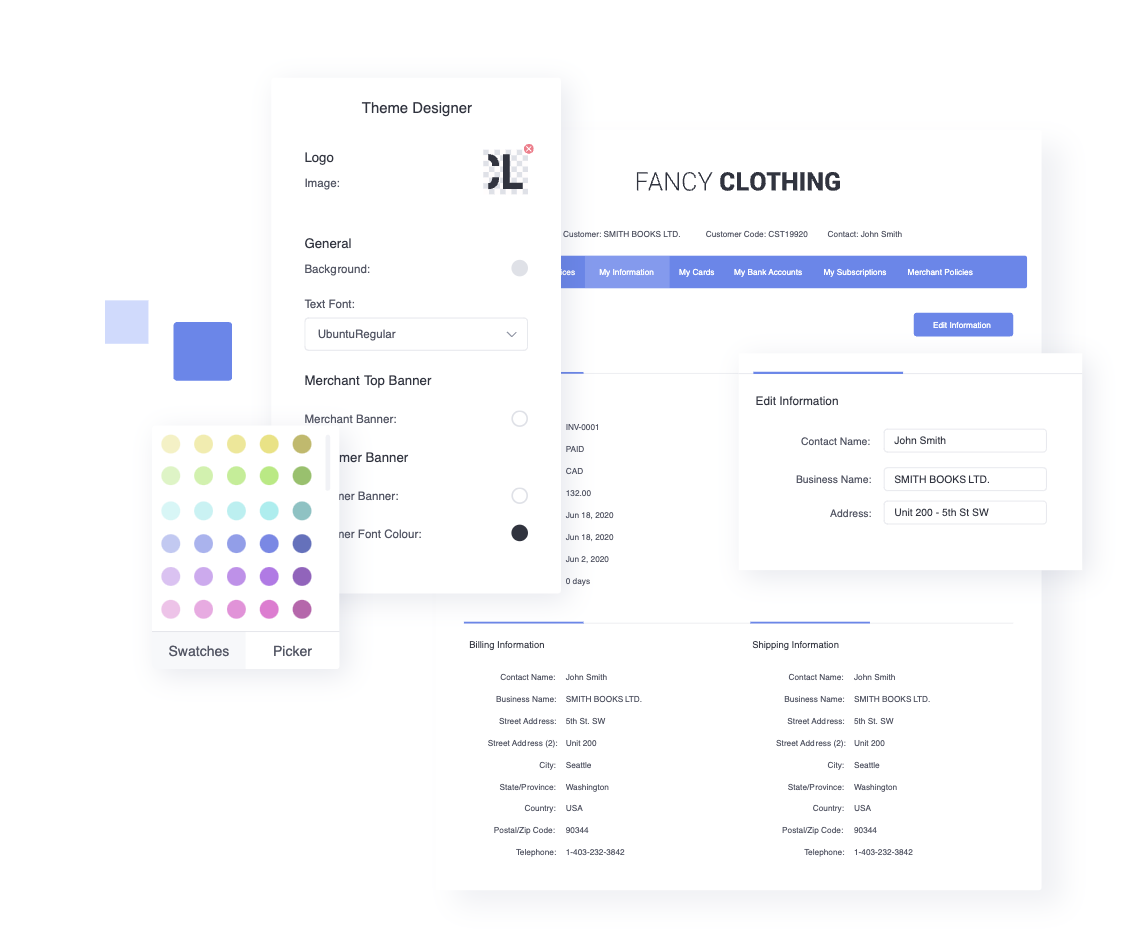

Helcim: Best for automated volume discounts

Overall Reviewer Score

4.48/5

Pricing & Contract

4.5/5

Payment Types

4.31/5

Sales & Account Management Features

4.38/5

User experience

5/5

User scores

4.2/5

Pros

- Interchange plus pricing

- Automated volume discounts

- Free credit card processing

Cons

- Limited business integrations

- Additional fees for AmEx transactions

- First payout takes two weeks

Why I chose Helcim

As a traditional merchant services provider, Helcim offers maximum stability to its users. But what I like most about Helcim is that it has built its platform around automation. Volume discounts are automated, every merchant account is automatically qualified for the in-person and online zero-cost processing program, and even B2B business information is automatically gathered for qualification for level 2 and 3 discounted rates.

- Zero-cost processing: Helcim’s Fee Saver program can support online, invoice, and in-person payments. Helcim can automatically detect the type of free credit card processing program available to use based on the card type/network and business location. Moreover, customers can choose to pay with ACH instead of a credit card to avoid the fees.

- B2B payment processing: Helcim offers both Level 2 and Level 3 credit card data processing. Level 2 is for all Helcim merchant account holders, and Level 3 is exclusive to merchants accepting Corporate, Purchasing, and Government credit cards. All of these are handled through Helcim’s virtual terminal.

- International payments with no currency conversion fees: Helcim can process overseas credit card payments with no additional currency conversion fees.

- Dispute management: Helcim has dispute management tools with a dashboard that displays dispute details, statuses of claims, and a link for uploading supporting documents.

- Monthly account fee: $0

- Card-present fee: Interchange plus 0.15% + 6 cents to 0.4% + 8 cents

- Card-not-present fee: Interchange plus 0.15% + 15 cents to 0.50% + 25 cents

- Domestic ACH transfers: 0.5% + 25 cents 5 per transaction

- American Express (card) transactions: Additional 0.10% + 10 cents

- Virtual terminal fee: $0

- Chargeback fee: $15 (refundable)

Square: Best for omnichannel payments

Overall Reviewer Score

4.42/5

Pricing & Contract

4.5/5

Payment Types

3.89/5

Sales & Account Management Features

4.06/5

User experience

5/5

User scores

4.67/5

Pros

- No chargeback or PCI compliance fees

- HIPAA-compliant

- Offers CBD program

Cons

- Flat-rate fees

- Custom fees available only by request

- Complaints of frozen funds

Why I chose Square

Square is an all-in-one point-of-sale (POS) solution with a built-in payment processing system. Its greatest advantage is that it can provide a full suite of tools for in-person and online selling, with minimal startup costs and no monthly fees.

Square offers a free POS system with every free Square Payments account. You can also build a free ecommerce website with its free Square Online website builder and Square automatically syncs your online and in-person orders and inventory.

Given all the tools you can get for free, Square provides the best value for new businesses, with minimal startup costs and no monthly fees. It is also compatible with small healthcare services because it is HIPAA compliant and merchants that sell cannabis products because it has a CBD program.

- Full-featured free account: What makes Square stand out from the rest is that it provides a full-featured business management software at zero cost. You can sign up for a merchant account, launch a business, and start accepting credit card payments with minimal upfront cost. A free account includes the following:

- Basic Square POS software

- Square payments processing

- Mobile POS app

- Basic ecommerce plan

- Payment gateway

- Virtual terminal

- Invoicing

- Customer directory

- Starter team management plan

- Magstripe mobile card reader

- Fund transfers: Funds are credited to your account as soon as the next business day, like Authorize.net. If you want same-day or instant funding, there is a 1.75% fee. However, if you sign up for a Square Checking account, instant fund transfers are free.

- CBD program: Through the program, Square can support businesses that sell CBD (Cannabidiol) products—hemp and hemp-derived CBD products that have less than, or equal to, 0.3% THC in most states within the US. Account requirements and fees are slightly different, with higher payment processing fees due to the risk involved.

- Monthly account fee: $0–$89 (includes POS software)

- In-person, mobile, and gift card payments: 2.6% + 10 cents per transaction

- Online payments: 2.9% + 30 cents per transaction

- Recurring billing and card-on-file transactions: 3.5% + 15 cents per transaction

- Keyed-in payments (virtual terminal): 3.5% + 15 cents per transaction

- ACH bank transfers: 1% with a $1 minimum transaction

- Invoiced payments: 3.3% + 30 cents per transaction

- Chargeback Fee: Waived up to $250/month

- Volume discounts: Custom pricing for any business processing over $250,000 in credit card sales.

Shopify: Best for ecommerce merchants

Overall Reviewer Score

4.29/5

Pricing & Contract

3.5/5

Payment Types

3.89/5

Sales & Account Management Features

4.53/5

User experience

5/5

User scores

4.53/5

Pros

- Shop Pay (one-click checkout)

- Waived Shopify transaction fees

- Customizable checkout pages

Cons

- Exclusive to Shopify platform; unavailable to other ecommerce platforms

- Ecommerce plan is required to use Shopify Payments (comes with monthly fees)

- User complaints of account holds

Why I chose Shopify

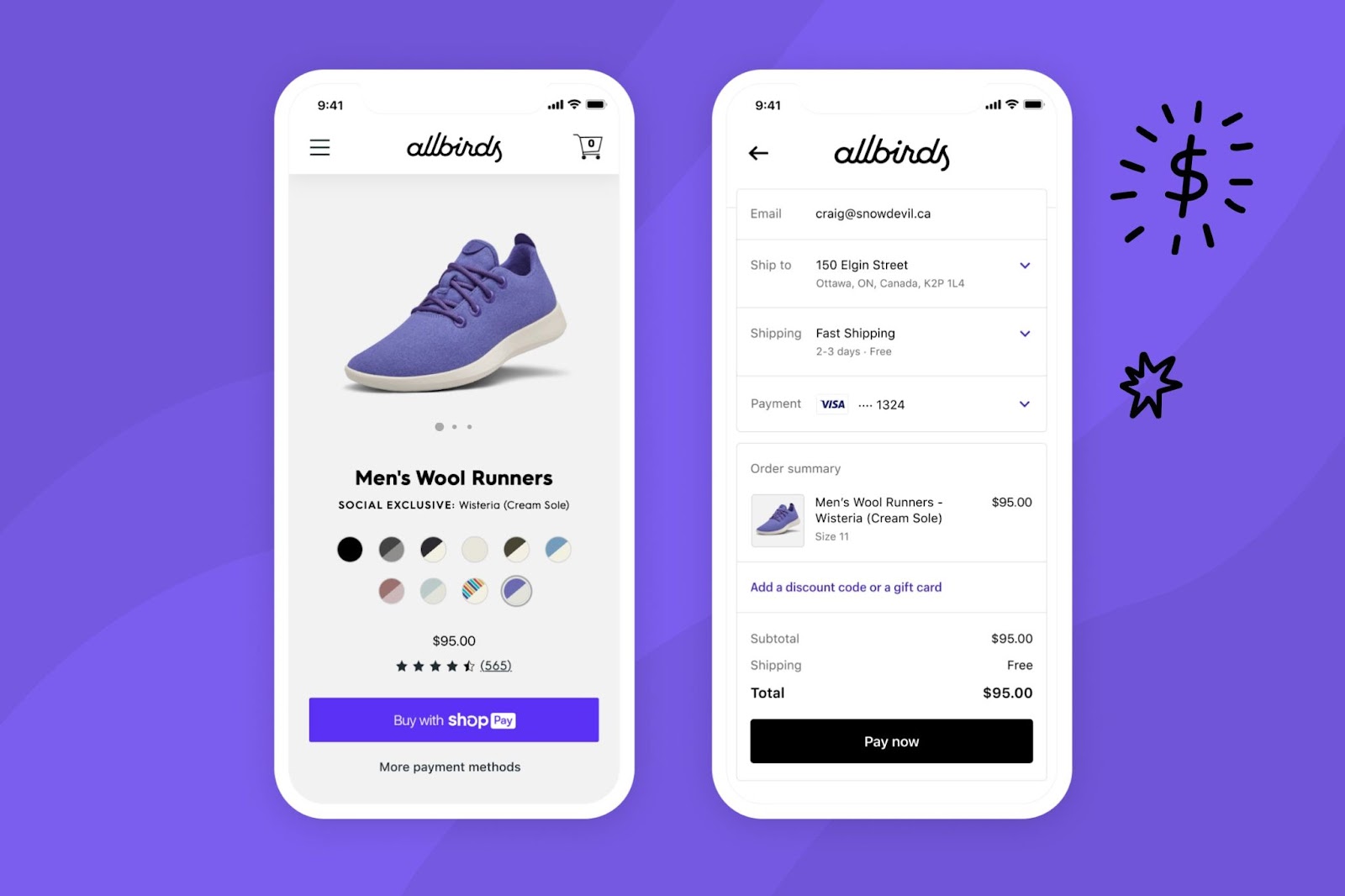

While Shopify Payments is exclusive to Shopify sellers, Shopify is the best ecommerce platform for real-world users and experts alike, making the system very ideal for ecommerce merchants.

I like Shopify Payments’ one-click checkout option, Shop Pay, and the various payment methods available for online merchants (even manual and in-person payments). Shopify is the standard for omnichannel and ecommerce point-of-sale (POS) solutions. I highly recommend going with Shopify Payments for online-first retail businesses.

- Payment methods: Shopify accepts in-person and online payment methods, including ACH and B2B payments. You can also create payment links, manually key-in payments, and send invoices.

- Virtual terminal: Accept over-the-phone purchases and sell products wholesale or by subscription through invoicing.

- Ecommerce checkout options: Allow customers to checkout from email carts, “Buy Now” buttons, quick response (QR) codes, and shareable links.

- Shop Pay: Shopify’s accelerated checkout feature lets customers sign up and securely save payment information for future transactions. Buy-now, pay-later options can also be enabled for purchases.

- Mobile app: Shop is Shopify’s customer-facing mobile app, available on iOS and Android devices. It allows shoppers to purchase your products from a mobile application.

Shopify Payments are available only when you subscribe to Shopify’s ecommerce platform. The fees vary based on the tier you subscribe to:

Starter plan:

- Monthly subscription fee: $5

- Online transactions (domestic): 2.9% + 30 cents

Basic plan:

- Monthly subscription fee: $39

- Online transactions (domestic): 2.9% + 30 cents

- Online premium card rates*: 3.5% + 30 cents

- Online international credit card rates: 1%

- In-person credit/debit transactions: 2.6% + 10 cents

- In-person manual credit/debit transaction rates: 3.5% + 10 cents

Shopify plan:

- Monthly subscription fee: $105

- Online transactions (domestic): 2.6% + 30 cents

- Online premium card rates*: 3.3% + 30 cents

- Online international credit card rates: 1%

- In-person credit/debit transactions: 2.5% + 10 cents

- In-person manual credit/debit transaction rates: 3.5% + 10 cents

Advanced plan:

- Monthly subscription fee: $105

- Online transactions (domestic): 2.6% + 30 cents

- Online premium card rates*: 3.1% + 30 cents

- Online international credit card rates: 1%

- In-person credit/debit transactions: 2.4% + 10 cents

- In-person manual credit/debit transaction rates: 3.5% + 10 cents

*includes commercial, corporate, and business cards and all cards issued by American Express.

Chargeback fee: $15 (refundable)

PayPal: Best for additional payment methods

Overall Reviewer Score

4.27/5

Pricing & Contract

3.75/5

Payment Types

3.61/5

Sales & Account Management Features

4.38/5

User experience

5/5

User scores

4.6/5

Pros

- Widely available, known and trusted platform by consumers

- Seamless online checkout integration

- Easy integrations

Cons

- Complicated pricing structure

- Account stability issues

- Unpredictable freezing of funds

Why I chose PayPal

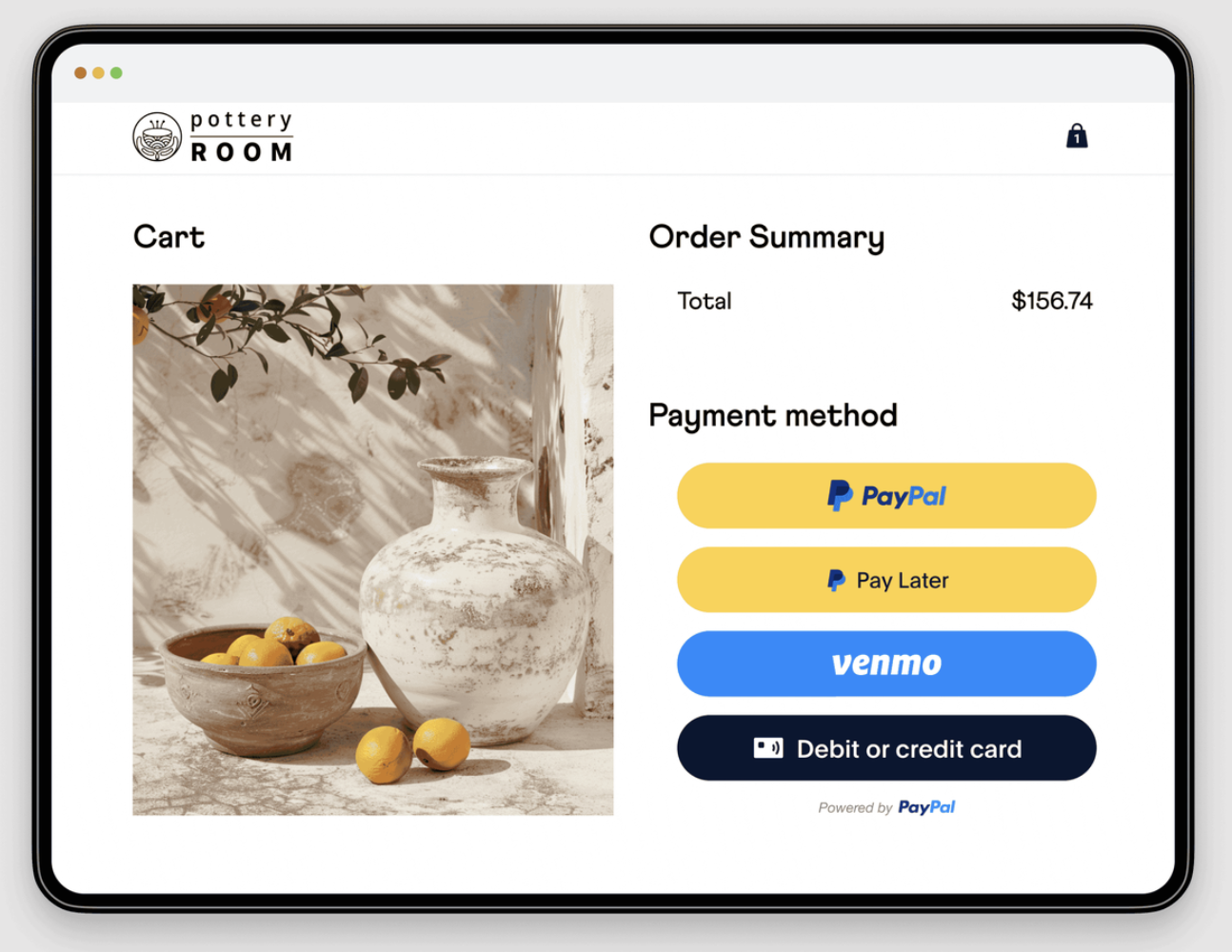

PayPal is a widely-trusted and used payment method all over the world. It is often used as an added payment method with other payment types. I find PayPal very easy to use, with Buy Now buttons for social media and checkout buttons for adding to your websites.

PayPal has its own BNPL tool and can accept cryptocurrency—the only provider that supports this on this list.

- Cryptocurrency payments: Unlike other providers on this list, PayPal accepts cryptocurrency payments. You can include a “Checkout with Crypto” as a payment method. When a customer chooses to pay in cryptocurrency, the crypto assets get converted to fiat currency and credited to your account.

- Buy Now, Pay Later (BNPL) options: PayPal has a native BNPL option that’s user-friendly for both businesses and customers.

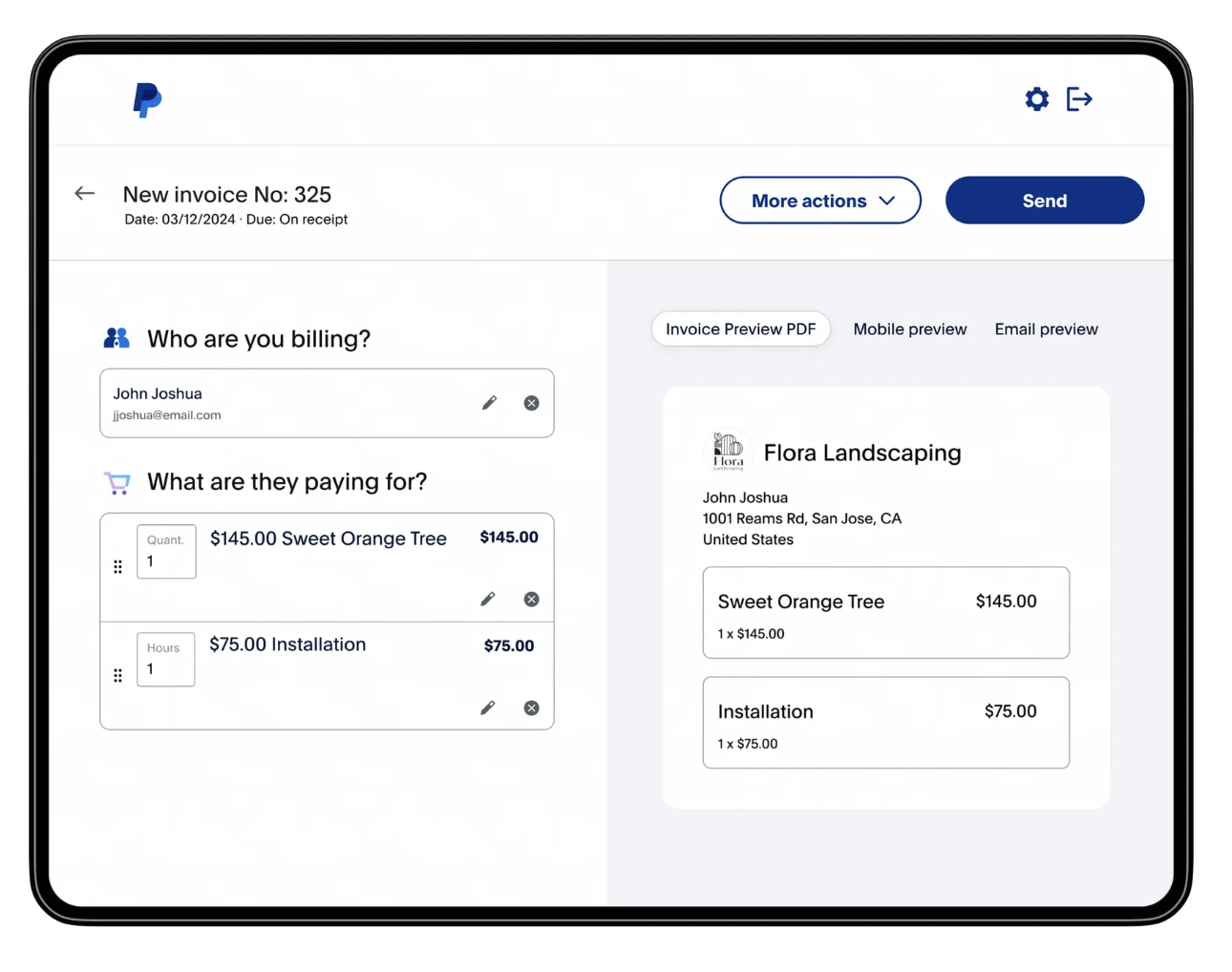

- Dispute resolution: There is a dispute resolution management center where the merchant and buyer can send messages to communicate, upload supporting documents and appeal a resolution. Funds are indefinitely put on hold until dispute resolution.

- Seller and fraud protection: PayPal has a seller protection program against claims and chargebacks and uses a two-sided network, a machine learning engine, and analytics to monitor suspicious transactions and stay up-to-date with existing fraud and evolving cyber threats.

- Monthly fee: $0–$30

- PayPal Zettle in-person transaction fee: 2.29% + 9 cents

- Online checkout transaction fee: 2.99% + 49 cents

- Keyed-in transaction fee: 3.49% + 9 cents

- Invoicing: 3.49% + 9 cents

- QR code payments: 2.29% + 9 cents

- Venmo payments: 3.49% + 49 cents

Chase Payment Solutions®: Best for fast deposits

Overall Reviewer Score

4.20/5

Pricing & Contract

3.75/5

Payment Types

4.31/5

Sales & Account Management Features

4.22/5

User experience

4.38/5

User scores

4.33/5

Pros

- Free same- and next-day funding

- Faster approval of international payments

- Fully HIPAA-compliant

Cons

- Chargeback fee can increase based on volume

- Maintaining bank balance required for same-day funding

- Add-on monthly fee for ACH transactions

Why I chose Chase Payment Solutions®

Chase provides traditional merchant account services and as a financial institution, you gain access to fast deposits and have higher chances of approval in accepting cross-border payments because of Chase’s strong connections to global banks. Chase offers the fastest deposit times for free among the providers on the list, with the caveat that you sign up for a Chase business checking account.

You get to enjoy the payment processing features other providers offer and the business and banking funding services a financial institution can provide.

Limited-time offer: Get $100 off the Chase Point of Sale (POS)SM Terminal. Visit Chase to learn more. Terms and conditions apply.

- Free same-day deposits and next-day funding: You can qualify for free same-day deposits depending on the service you use at no extra cost, unlike Square, which charges an extra fee for the same feature.

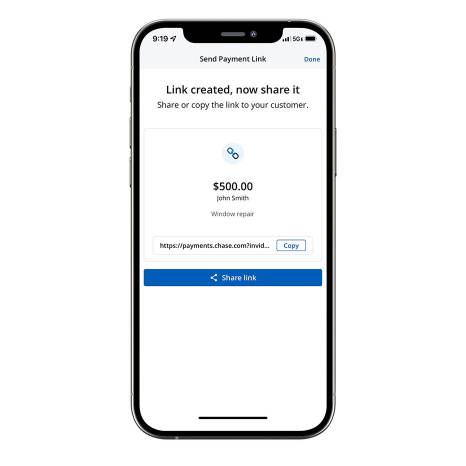

- Quick Accept: This feature lets you accept credit card payments in person and over the phone and manage transactions across multiple devices using one sign-in.

- Virtual terminal and B2B payments: Orbital is Chase Payment Solutions’® proprietary virtual terminal that can support B2B payments, is equipped to accept cross-border payments, and has Level 2 and Level 3 credit card processing.

- Business funding and banking: As a direct processor, Chase offers a complete suite of business banking services, from checking accounts to loans to credit cards. It also offers business services like global wire transfers.

- Monthly fee: $0–$15*

- Card-present transaction fee: 2.6% plus 10 cents

- Card-not-present transaction fee: 2.9% plus 25 cents

- Keyed-in transaction fee: 3.5% + 10 cents

- ACH processing fee: $25/month for 25 transactions, 15 cents for additional

- Chargeback fee: $25 to $100 per transaction depending on dispute volume

*Access to same-day funding with a Chase Business Checking account requires maintaining a $2,000 monthly balance. Otherwise, a monthly service fee of $15 will be imposed.

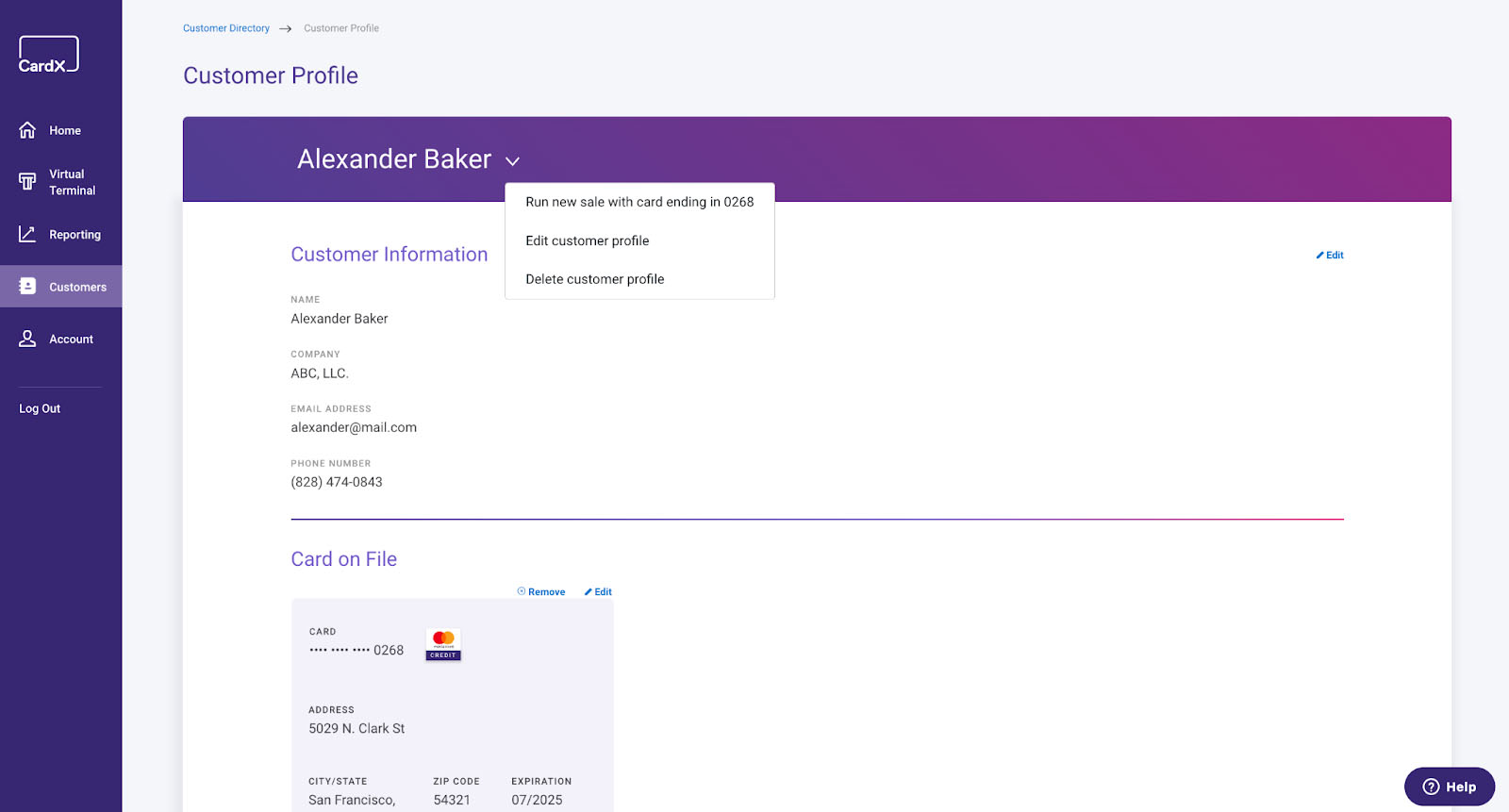

CardX: Best for surcharging

Overall Reviewer Score

3.51/5

Pricing & Contract

4/5

Payment Types

3.06/5

Sales & Account Management Features

3.13/5

User experience

4.38/5

User scores

3/5

Pros

- Fully compliant and automatic credit surcharging for online and in-payment transactions

- Auto-detection of debit and credit cards

- Built-in virtual terminal and subscription management tools

Cons

- Lacks same-day funding

- Lacks invoice customization tools

- Does not accept cross border payments

Why I chose CardX

CardX offers surcharging programs for online and in-person transactions, provides invoicing and subscription management features, a CRM tool, and virtual terminal.

I like how CardX is an expert on surcharging compliance. It doubles down on compliance to provide merchants with a surcharging program and even conducts free merchant training. It is fully compliant with federal and local regulations in all states where credit surcharging is legal. Mastercard appointed CardX as its official surcharging partner and provides merchants with the Mastercard Click-to-pay feature for their website checkout.

I also like how its subscription management tools are integrated with CardX’s customer profiles, so you can easily track and manage accounts receivables.

- Compliance on surcharging: CardX covers every card network rule on credit card surcharging and is Mastercard’s official surcharging partner.

- Payment methods: CardX accepts debit cards as a preferred alternative payment method, and it can automatically detect whether a credit or debit card is used. You can create and send invoices with embedded checkout forms and manually process payments through a virtual terminal.

- Customized online checkout: CardX provides Lightbox so you can create simple and customized online checkouts and integrate with your ecommerce platform.

- Reporting tools: One of CardX’s outstanding features is its reporting functionality—sales and deposit records connected with customer profiles.

- Pre-programmed card terminals: To collect payments in person, CardX provides pre-programmed stand-alone card terminals that can also be used alongside POS systems.

- Monthly Account Fee: $29–$199

- Card-Present Fee: From 2.91% for debit card payments

- Card-Not-Present Fee: From 2.91% for debit card payments

- Chargeback Fee: $0

A Guide To Accepting Payments Online

Accepting payment online involves several steps, from identifying priorities, choosing a provider, to integrating that provider with your website and systems. The process also varies depending on your business requirements, needs, and the provider’s regulations. Overall, the steps involved are as outlined below:

- Identify your business needs. Determine what types of payments you need to process and whether your business just needs one-time payments or the ability to do recurring billing, manual payments, and more. If your business operates in multiple countries, you might need to support payments in different currencies. These requirements will determine your next steps.

- Choose a payment processor. Once you determine your business needs, go with a processor that can support all your requirements and integrate with your existing business systems with minimal friction. We also outline all the considerations you need to look into when deciding on a payment processor in the next section.

- Integrate the payment processor into your website. Once you have chosen a provider, you need to create an account and go through the verification process. Once approved, you can integrate the processor into your website. Most provide prebuilt plugins or APIs for integration, but this step will vary depending on your website and the provider you choose.

- Configure payment settings. Once successfully integrated, it’s time to set your payment options. Set up the payment methods you are willing to accept. Now is also the time to set up subscription models, BNPL options, and recurring billing methods.

- Test the system. Payment processors typically have testing modes to help simulate payment transactions and ensure everything works properly before you launch and go live.

- Launch the payment system. Once it is tested thoroughly, it’s time to go live! Start accepting payments and regularly monitor transactions. Most provide dashboards and tools to help with monitoring sales and handling disputes or chargebacks.

- Consistently adhere to compliance and accounting requirements. Once it is launched, you need to stay on top of compliance regulations and PCI DSS standards.

Choosing the Best Online Payment Processor For Your Needs

The best online payment processor will depend on your businesses. When choosing an online payment system for your business, consider the following:

- Security: Security is crucial when accepting payments online. Ensure your provider is PCI-compliant. The good providers also use the latest encryption technologies that protect credit information from theft.

- The industry risk of your business: There are payment processors that don’t cater to specific industries because of the risk involved in accepting certain payments. Examples include gas stations (high rates of fraudulent transactions), telemarketing sales (high rates of chargebacks), and sales that are regulated under federal law, like firearms.

- Accepted payment methods: The payment processor should support the payment methods your business needs to process. For example, if you process payments via phone or invoicing, shortlist systems that support these options.

- Integrations: Integrations allow you to automate and efficiently coordinate your business systems. As a rule, you must be able to integrate your processor with your shopping cart. Check if your existing software (accounting, CRM, ecommerce platform) has native integrations with your shortlist.

- Contract length: Some payment processors offer month-to-month contracts without cancellation fees while others don’t. Study contract agreements, especially if you own customer data if you choose to transfer providers—there are services that allow it, some don’t. For example, if you have a loyalty program and switch providers, that would mean you need to start again from scratch.

- Customer support: Live 24/7 support is ideal but may not be a necessity for all businesses. However, if your business accepts keyed-in payments from across the country, takes mobile payments at weekend events, or operates outside business hours, an issue with processing payments can come at various times and you risk loss of revenue if the issue isn’t resolved promptly.

- Timeline for payouts or fund transfers: Generally, the time it takes to receive funds from online payments should be short—next-day payouts are standard. However, same-day deposits can be important for some businesses. Most providers offer same-day payouts with added fees, while others don’t have the capability to provide this need. If so, factor in the fees involved with same-day payouts and estimate the added cost per month.

- Over all cost (fees, charges, monthly subscriptions): The overall cost of payment processors includes transaction fees, monthly fees, chargeback fees, and less-obvious costs such as membership fees, setup costs, PCI compliance fees, and cancellation fees. When comparing providers, look into their setup fees, hidden charges, refund fees, and international transaction fees. Check if it can also provide interchange-plus pricing instead of flat-rate pricing for processing fees, especially if your business has a high volume of monthly transactions.